Personal Finance in Switzerland: What Is the Swiss National Interest Rate?

Like many other countries, Switzerland has a central bank and a national interest rate. But what does this mean, and how does it affect personal finance in Switzerland? Let’s have a closer look at the Swiss national interest rate and what it might mean for you as a resident.

The Swiss National Interest Rate Explained

The national interest rate is set by the Swiss national bank. It is the rate that commercial banks pay the national bank when they borrow money. When the rate goes up or down, commercial banks eventually pass on the changes to their customers. As a result, borrowing money either becomes cheaper or more expensive. Typically, the national interest rate is determined once every three months.

Is the National Interest Rate the Same as the Mortgage Reference Interest Rate?

The SNB publishes two different rates. The national interest rate is a broader measure of the economy, and it affects the cost of borrowing and the level of economic activity in Switzerland. The mortgage reference interest rate is more specific. It’s the average of all mortgage interest rates in Switzerland, and it mainly affects mortgages and rents.

Further reading: What Is the Swiss Reference Interest Rate?

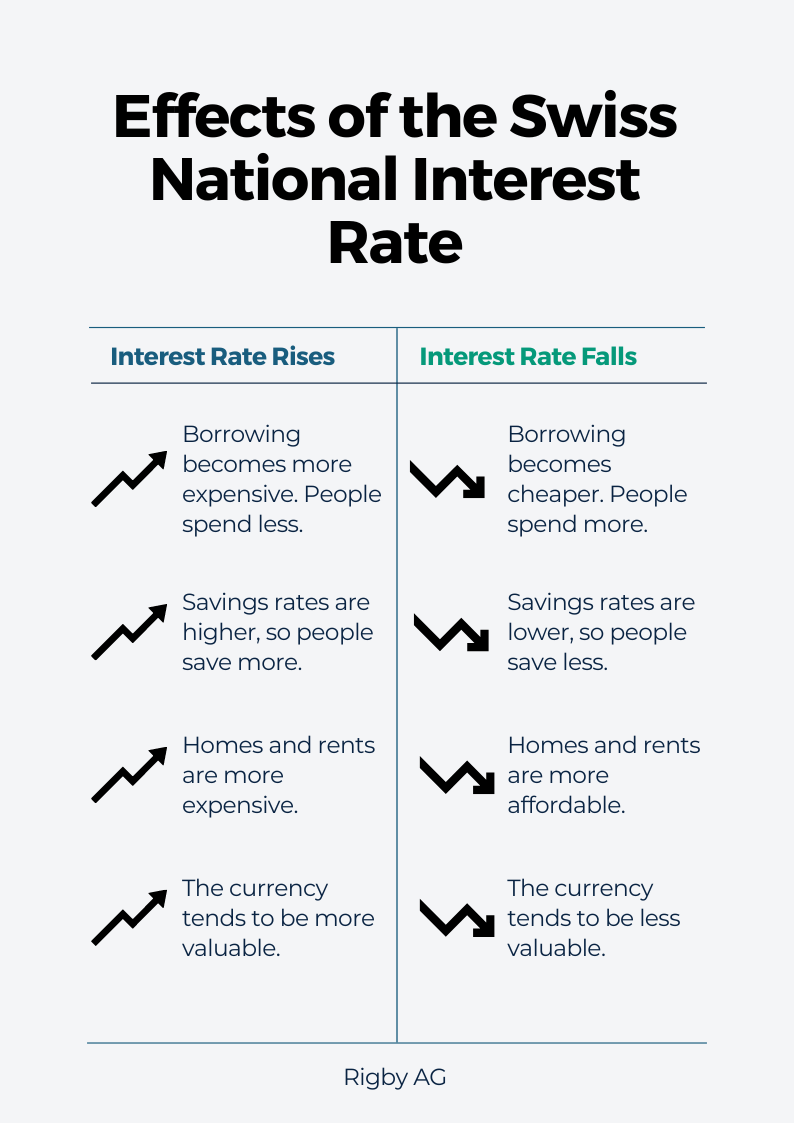

Effects of the National Interest Rate on Personal Finance in Switzerland

The national interest rate affects public decisions, corporations, and individuals’ personal finance in Switzerland. It is an important measure of how the economy is doing and what the current focus is.

Consumers

When prices rise, the SNB can increase the interest rate to slow down the economy and halt excessive inflation. This works because banks, and therefore individuals, have to pay more to borrow money as a result of an interest rate increase. This means they have less money to spend, demand is reduced, and prices of goods drop.

On the other hand, a slow economy can be stimulated by decreasing the interest rate. When banks — and therefore consumers — can borrow money more cheaply, they are more likely to spend.

Savers

Savers benefit from rising rates because they receive more interest on the money deposited. When the national interest rate was negative in the years preceding 2022, many people had to pay to keep their money in the bank. Now that interest rates are higher, the banks once again pay interest.

Investors

The opposite is true for investors. Interest rates are raised to slow down the economy and lowered to speed it up. Therefore, investors can expect better returns when interest rates are lower, since companies are likely to borrow more money and grow faster during low-interest periods.

Homeowners

The lower the Swiss national interest rate, the lower the mortgage rates. However, the effect often can’t be felt for several years, as many people have fixed mortgages. This is why the mortgage reference interest rate takes longer to change than the national interest rate.

Tenants

Rents are linked to the mortgage reference interest rate. If it goes up, the landlord can demand a rent increase. If it goes down, the tenant can ask for their rent to be decreased.

Although the mortgage reference interest rate is linked to the national interest rate, it is much slower to change, so an adjustment of the national interest rate doesn’t immediately translate to higher or lower rents.

The Swiss Franc Exchange Rate

When banks borrow less money, the total amount of the currency in use is reduced, and the currency becomes more valuable. That’s why high interest rates typically have a positive effect on the value of a currency. However, the interest rates of the other countries also have to be taken into account. If they rise or fall at approximately the same rate, the effect on the exchange rate may be minimal.

What Is the Current Swiss National Interest Rate?

The Swiss national interest rate was negative for many years, but it is now once again positive. At the moment, it’s 0.5%, down from 1.75% in 2023 and early 2024. The next update is expected in March.

The Swiss national interest rate can have a significant effect on individuals’ personal finance in Switzerland. It affects savings, investments, mortgages, rents, and exchange rates. If you want to learn more about living and working in Switzerland, download our comprehensive ebook and sign up for the monthly Rigby AG newsletter now. We regularly publish and share information about Swiss finances and the job market.